US influence in global advertising

3 top-of-mind issues for US advertisers in 2021 that don’t translate elsewhere (yet)

The United States is the largest global consumer market, with 328 million people, roughly 25% of the world’s household consumption, and $20.8 trillion in GDP. Many of the tools and technologies that define today’s global internet originate in the United States.

The US media market rings in at more than twice the size of the next largest one – China’s – and commands $225.79 billion in media ad spend (compared to China’s $105.25 billion, per eMarketer data). You’d have to roll up the next six and a half largest national media markets to get close to market-size parity.

The US market is so dominant and influential that many conversations taking place among digital marketing and advertising professionals globally actually revolve around challenges that are important in the United States – though not necessarily as relevant beyond its borders. At least not yet.

It’s worth paying attention to what’s happening in the world’s largest advertising market. What begins in the United States often trickles to other regions in unexpected ways, and for companies in other markets, these challenges represent potential opportunities to step in with their own solutions.

Three topics in particular are coming to a head in the United States this year: tensions between walled gardens and the open internet, the role and opportunity for connected/convergent television (CTV), and regulatory activity.

These three themes will be top of mind for US marketers in 2021. Here’s what you need to know.

The tug of war between walled gardens and the open internet

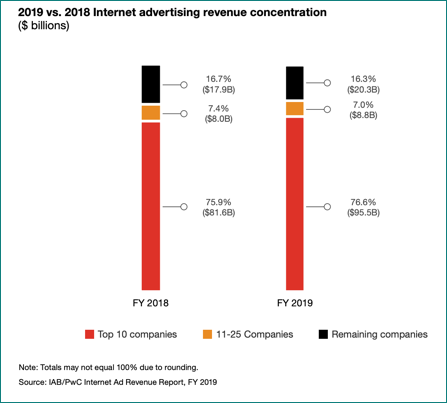

US digital ad revenue in 2019 alone reached $124 billion, which translates to approximately 91 billion pounds or 103 billion euros. Yes, that’s with a B.

The market has grown healthily, by double digits year over year, but beneath this dramatic expansion lays a hyper-concentration of revenue: The IAB and PwC report found that 83.6% of all revenue goes to the top 25 largest companies. There’s further stratification here, with 76.6% of all 2019 revenue being generated by the top 10.

The top 10 quickly transform into the top three: Google, Facebook, and a rapidly gaining Amazon. In other markets, the top two are usually the same, with the third slot often, for the time being, occupied by a regional competitor or a local media conglomerate.

Walled gardens are incentivizing marketers to spend more by providing tools and insights that the open internet, mainly powered by programmatic and many independent players of various sizes, is struggling to match. Walled gardens make buying easy at the expense of transparency. (Measurement scandals are frequent, and without independent verification buyers have few options but to trust platforms implicitly.) This in turn creates a highly fragmented media universe with little coordination from garden to garden. With the pending retirement of third-party cookies and Apple’s rollout of the App Tracking Transparency (ATT) privacy framework, the business case for the open internet seems to be getting weaker and weaker. For example, JPMorgan Chase famously cut the number of websites on which it advertised from 400,000 (!!!) to 5,000, with no decline in business performance (though it later reportedly increased the number of websites to about 10,000). Similarly, P&G slashed spending on digital advertising by $200 million, with little impact on business. In markets with stronger privacy and data protection – an area where the United States is lagging – this tension between walled gardens and the open internet doesn’t manifest as such an existential issue (although revenue concentration as a trend continues to favor walled gardens).

Connected and convergent TV (CTV)

Few will be able to escape the hottest topic du jour this year: CTV.

Since the dawn of digital advertising in the mid-1990s, we had a target in mind. Early digital champions talked of a world in which digital budgets rivaled television advertising budgets; to TV executives that must have sounded like a pipe dream. Slow to adopt TV anywhere, those same TV execs seemed to miss consumer shifts away from paid broadcast and cable and toward other forms of entertainment. Paid TV households continue to drop; In 2020, we were down to 82.9 million households (or 65.2%), per eMarketer data. By 2023, we can expect that number to shrink to 72.7 million households, or 56.5% of the population. With fewer eyeballs, ad spend is also shrinking, projected to decline from 29.4% in 2019 to 22.8% of all media spend in 2023.

Changes in media consumption caused ad spend on linear TV and digital channels to equalize in 2016 and flip. TV ad spend has since remained enviously large yet essentially flat, with digital increasing its share of budgets and consumer attention. With US consumers canceling cable subscriptions, TV advertisers have followed the eyeballs to digitally originating TV, including SVOD and AVOD. Enter CTV and the opportunity to take more share from still-healthy linear TV budgets and execute it with digital inventory (where the consumers are).

In other markets CTV isn’t such a do-or-die issue. Cable TV subscriptions are a far better deal for consumers in Europe and Asia, where there is less of a need to cancel their subscriptions than their US counterparts. Outside the United States, CTV is more about consumer flexibility and a better viewing experience and less about a fundamental reimagining of the underlying commercials that fund television. As a result, local and regional solutions may serve these markets better than imports or platforms from the United States.

Privacy and regulation

Since the inception of direct marketing, the United States has enjoyed a very liberal, opaque, and unregulated data market. With greater perceived risks of digital data misuse, this environment is rapidly changing. More than a half-dozen states have indicated their interest in state-level GDPR-like privacy structures largely related to digital datasets; most notable is California’s Consumer Protection Act (CCPA), which went into effect in January 2020, and its successor California Privacy Rights Act (CPRA), which will go into effect in 2023.

But this state-level activity is like building a house without the foundation. The US market's size is what makes it so strong and lucrative, yet these state-level privacy laws risk discombobulating the national market and making it difficult for companies to comply with disparate rules. A basic privacy framework at the federal level would be a welcome step toward removing some of the privacy-related uncertainty that’s currently present in-market. With a change in presidential leadership, the signals from the new Biden administration suggest that it will take on the mantle of data protection and possibly scale up the state-level initiatives to the federal level. Without this, US companies will find it challenging to lead on privacy.

The other regulatory angle is antitrust. With walled gardens commanding such an outsize portion of revenue, the question of fair competition and monopolies naturally arises. In October, the House Judiciary Committee issued its report on the state of competition in digital markets. The US Department of Justice and state attorneys general subsequently filed multiple lawsuits against Google and Facebook alleging anticompetitive business practices. But scrutiny of the tech giants has been harsher in Europe, so these longer-term conversations will have implications for both sides of the pond. Non-US markets don’t really have a direct stake here, other than observing and knowing that the ramifications of these antitrust cases are likely to eventually affect their markets.

Why should you care?

Think of US market influence as resembling an iceberg, with 90% being invisible, making it crucial for global companies to at least be mindful of US issues that may filter through to other markets. Many strategy and product decisions in platforms and software tools are modeled primarily for the US market; this creates an opportunity to take advantage of where the US market diverges from the needs of your local market and develop specifically to solve non-US issues. Similarly if you’re a US-based innovator or operator take care to identify the issues that are specific to the US market and don’t translate as well to other regions.

One Question:

With the walled gardens dominating global ad spend, where are there opportunities for non-US ad tech and mar tech companies to complementarily plug into larger markets, and where can they be competitive?

Dig deeper:

eMarketer’s ad spending outlook

US Pay TV Suffers Historic Cord-Cutting

The IAB’s Full-Year 2019 Internet Advertising Revenue Report

"Investigation of Competition in Digital Markets" report from the House Judiciary Committee's antitrust panel

These US Antitrust Cases Facing Google, Facebook and Others - WSJ

Thanks for reading,

Ana & Maja

Enjoyed this piece? Share it, like it, and send us comments (you can reply to this email).

Who we are: Sparrow Advisers

We’re a results oriented management consultancy bringing deep operational expertise to solve strategic and tactical objectives of companies in and around the ad tech and mar tech space.

Our unique perspective rooted deeply in AdTech, MarTech, SaaS, media, entertainment, commerce, software, technology, and services allows us to accelerate your business from strategy to day-to-day execution.

Founded in 2015 by Ana and Maja Milicevic, principals & industry veterans who combined their product, strategy, sales, marketing, and company scaling chops and built the type of consultancy they wish existed when they were in operational roles at industry-leading adtech, martech, and software companies. Now a global team, Sparrow Advisers help solve the most pressing commercial challenges and connect all the necessary dots across people, process, and technology to simplify paths to revenue from strategic vision down to execution. We believe that expertise with fast-changing, emerging technologies at the crossroads of media, technology, creativity, innovation, and commerce are a differentiator and that every company should have access to wise Sherpas who’ve solved complex cross-sectional problems before. Contact us here.