Revisiting the Streaming Wars

How have our grades aged?

This month marks the end of an era: Ana is canceling her Max streaming subscription.

She's been a subscriber of some variant of HBO’s streaming offering ever since its launch back in 2010. But with Apple TV stealthily replacing the quality of Max in her household, on top of Max embracing decidedly non-premium content, Ana will join the growing ranks of consumers who are abandoning some of their streaming plans.

The streaming wars have entered a new stage marked by churn, price hikes, and a crackdown on password sharing. At the same time, streaming has never been so popular — at the expense of linear TV viewing, which fell below 50% last month for the first time.

The US streaming subscriber churn rate was 6% in July, up from 4.7% a year ago. Churn is a huge headache for streaming services because it pressures them to acquire new customers, which often requires expensive marketing costs. Churn increased for every streaming service in July except for Netflix, likely because of its new policy to curb password sharing.

The move helped Netflix to add net new subscribers in Q2, and others like Disney plan to follow suit. Before the crackdown, about 100 million Netflix subscribers shared their passwords with people outside their households, according to the company. Analysts expect half will stick around and open their own new accounts.

About a quarter of Netflix’s new subscribers last month chose its new ad-supported tier, and the company is hoping to expand this cohort. It's not alone. The major ad-free streaming services are rising nearly 25% a year, according to The Wall Street Journal. That includes Disney+, Hulu, Peacock, Max, Paramount+, and Apple TV+. (Even with the price increases, streaming TV is still less expensive than many cable bundles, as some would like us to believe.)

(This story also has some good charts)

Many are raising these prices to nudge people to cheaper ad-supported options, which are more lucrative in a space where it takes big bucks to play. Disney, Netflix, Paramount, Warner Bros. Discovery, and NBCUniversal have all acknowledged that average revenue per user is greater for their ad-supported tiers vs. ad-free.

Aside from price, content is one of the largest factors driving loyalty among streaming audiences. The ongoing writers' and actors' strikes will put a crimp on new content coming from the US, so streaming services are going to have to get creative and look to other international markets for content, including Turkey, LatAm, and Nordic nations.

Let's revisit one of our favorite Ones: Grading the streaming wars.

Netflix’s most recent earnings season brought two big surprises: its first significant subscriber loss — 200,000 — and an announcement of a soon-to-be-coming advertising tier. The company that spent years eschewing ads had a sudden change of heart, understandably so since the streaming landscape looks much different today than it did just three years ago, when Netflix only competed with sleep for its users' attention.

In fact, for the better part of the last 15 years, Netflix was the clear streaming leader and category definer, with virtually no competition. Sure, there were smaller offerings, such as HBO’s various experiments with online streaming services (RIP Now, Go, and, likely soon, Max). Disney also started kicking the tires back in 2015 when it began testing DisneyLife in the UK. But other than that, Netflix pretty much had a wide-open field all to itself until companies with large content libraries and balance sheets began looking at streaming as cord-cutting in the traditional TV world accelerated.

Thanks for reading Sparrow One! Subscribe for free to receive new posts and support my work.

Subscribed

But streaming is not for the faint of heart. The cost of entry remains significant, and it’s unclear if there will be a clear winner, which is a very different environment than 2007, when Netflix launched its streaming offering. Instead, we’re going to likely see a lot of companies nibbling at each other's margins and audiences. The later they enter the streaming wars, the less wallet share, cultural cachet, and — more importantly — share of attention they can grab. We expect consumers to choose roughly three paid subscription entertainment services as outlined in our Rule of Threes thesis. Consumers are not going to endlessly subscribe to streaming services; their time is limited by the number of hours available every day for entertainment, which itself is constantly diversifying with new forms of gaming, social media, and IRL activities. On the other hand, content is becoming commoditized; most streaming services that people already have offer “good enough” libraries. Don’t want to subscribe to Paramount+ so you can watch a soapy Western like “1883”? No problem, you can watch “Longmire'' on Netflix instead. This creates a paradox where streamers still need to invest heavily in content as if it were a differentiator, when in reality, it’s quickly trending toward becoming a commodity.

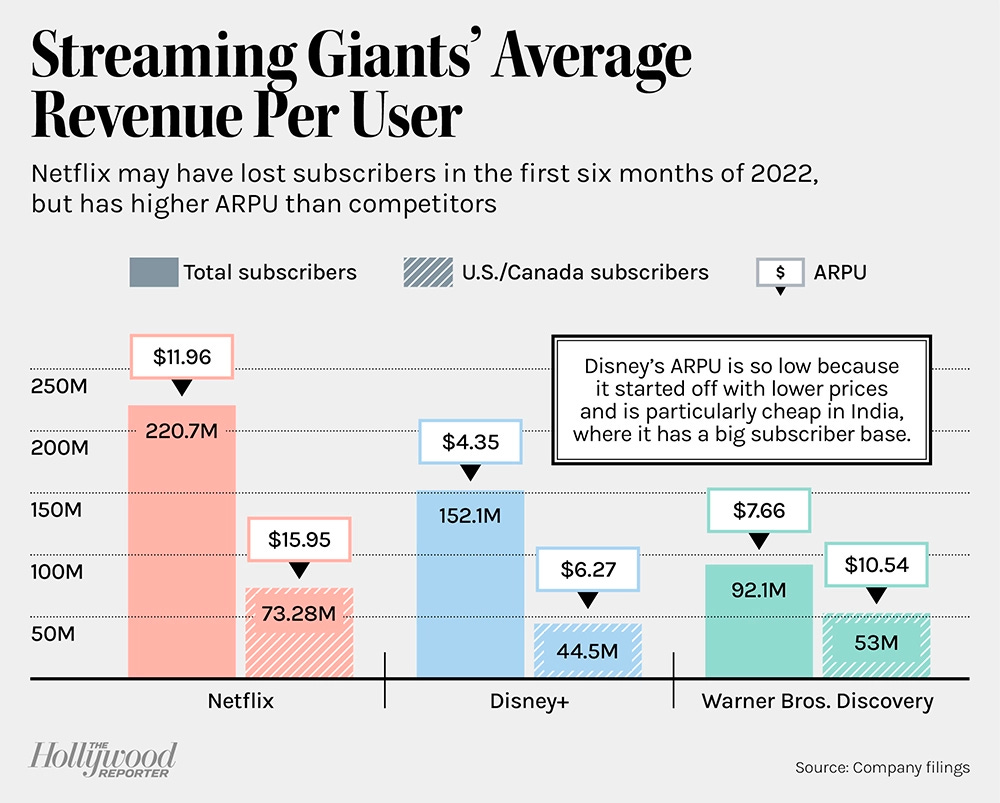

We’ve long thought that it would be inevitable for Netflix to lose market share because the quality of competition is so significant. Other streaming services are undeniably making inroads. In its most recent earnings report, Disney revealed that Disney+ subscribers reached 152.1 million, for example, but that includes 58.4 million from Disney’s Hotstar partnership in India, which adds significant headcount at low average revenue per user (ARPU): $1.20. Disney’s global ARPU is $4.35, compared to $11.96 for Netflix.

As we outlined in Rule of Threes, monetization for these services is generally either subscription, subscription + ads, ads only, or bundling with something else consumers want, like other streaming services in Disney’s case or a service like Amazon Prime, which can improve stickiness. That’s an issue in streaming, where churn keeps growing: Nearly 20% of premium service subscribers had canceled three or more subscriptions in the past two years, an increase from 6% in 2020. Is churn a feature or a bug of the streaming ecosystem? While loyalty as a concept made sense when there were annual contracts, hardware, and cable/satellite pricing incentives for longer commitments, what is the expectation of loyalty to a particular streaming service if those and similar incentives are absent?

Moving forward, we see several levers that streaming services can pull to differentiate: UX, reach, market opportunity, ad experience, and cost, to name a few. To gauge how the different services approach these levers, we examined different categories of players — Category Creators, Platform Plays, Fast Followers, and AVOD Pioneers — and included a deep dive of two representative players from each group, with scores based on these attributes. How do leading services stack up against each other?

CATEGORY CREATORS

These streaming services differentiate on a premium user experience and content quality primarily through a streaming video on demand (SVOD) tier.

NETFLIX’s simple interface makes it easy to binge-watch new content seamlessly across devices. Personalization on the platform is key, with a recommendation algorithm that users can help train by giving content a thumbs up or down. Netflix has spent billions creating content in local languages in key markets, including India, Eastern Europe, and Latin America. Global subscribers reached 220.67 million in Q2 2022, with roughly a third — 73.28 million — based in the US and Canada. US subscriptions range from a $9.99 per-month basic plan to $19.99 per month for four screens. Netflix spent $17 billion on content last year and plans to maintain that level of investment for the next few years. Its content helped the company capture 160 Emmy nominations in 2020, and seven Oscar Best Picture nominations since 2018. Netflix plans to introduce a lower-cost AVOD option in early 2023 after selecting Microsoft as its partner for ad sales and technology support. As we've previously written, Netflix has an opportunity to redefine ad-supported video on demand and reimagine the advertising experience, from new interactive ad units to leveraging its excellent recommendation algorithm to match views to ads that are the most relevant. Its GTM strategy seems to be periodically leaking bits of information to sustain excitement in its AVOD tier.

(A quick note about our mostly qualitative scoring methodology: Each component is graded on a scale of 1-10, with a maximum score of 60, not including bonus points for cultural impact and other intangibles).

Our score: Netflix set the standard for a clean and quick player, UX, scrubbing, and autoplay. It gets bonus points for becoming a verb — “Netflix and chill” — and inventing binging, an entirely new category of consumer behavior.

• UX: 9.5

• Reach: 9

• Market opportunity: 5

• Ad experience: ¯\_(ツ)_/¯

• Value: 7

• Content investment: 10

• Cultural impact bonus points: 10

Total score: 50.5

HULU was the first streaming service to use “Plus” as part of its name when it rolled out its subscription service in 2010. The service offers great UX, content, and ad experience but has a funky ownership structure: Disney became a majority stakeholder in Hulu when it bought most of Fox in 2019, and Comcast owns the remaining 33%. There is a lot of uncertainty in whether Disney will pick up the remaining stake in 2024. Hulu has 46.2 million paid subscribers in the US, according to Disney’s most recent earnings report, including 4 million live TV customers. It is Disney’s fastest-growing US streaming service, outpacing subscriptions for Disney+ for the majority of the last two years, driving more users to the House of Mouse than Star Wars or Marvel. Hulu will increase prices in October 2022 to $14.99 for its ad-free tier (from $12.99 currently) and $7.99 for its ad-supported option (from $6.99 currently). Hulu’s ad load for its original content rang in at a low 7.4 per show or 12 ads per hour. Hulu charges CPMs of $20 to $33 for ads that run for 10 minutes each hour. Content costs for fiscal Q1 were $1.83 billion.

Our score:

• UX: 9

• Reach: 6

• Market opportunity: 4

• Ad experience: 9

• Value: 8

• Content investment: 5

Total score: 41

Honorable mentions: Apple TV+, a recent entrant that seems to be trying to position itself as the home of prestige television. No ad tier yet, with advertising efforts that seem to currently be focused on live sports content. Watching Apple TV+ reminds us of HBO’s old “It’s not TV, it’s HBO” slogan: Will Apple TV+ become the prestige HBO of its era?

PLATFORM PLAYS

These services are offered by large walled garden platforms such as Amazon and Google, adding to their ad revenue and data pipelines.

AMAZON Prime is a premium SVOD service, but people generally become subscribers as part of their Prime membership, not for Amazon’s video library. The platform also offers ad-supported video services such as Twitch, live sports like Thursday Night Football, and Freevee, which was rebranded from IMDb TV in April 2022. Prime’s interface is finally getting a redesign after complaints that it was too busy and overwhelming, and it will add a top 10 ranking that resembles Netflix’s. Amazon’s 200 million-plus global subscribers have access to Amazon Prime Video; Amazon doesn’t break out numbers but has said that it has 120 million monthly active users for its ad-supported video content. Amazon Prime membership costs $14.95 per month, or $139 per year. Amazon spent $13 billion last year on film, TV, and music content, an 18% increase from 2020. For its AVOD inventory, Amazon charges a CPM in the range of $20-32, with extra fees for targeting and ad measurement. FreeVee’s ad experience is interesting because the ads promote products that can be purchased through Amazon. The ads share a similar aesthetic with Western actors, as if they are produced by the same agency.

Our score:

• UX: 8.5

• Reach: 8

• Market opportunity: 5

• Ad experience: 6

• Value: 6

• Content investment: 8

Total score: 41.5

YOUTUBE began streaming more than 4,000 free, ad-supported TV episodes from “Hell’s Kitchen,” “Heartland,” and other shows in March, in addition to more than 1,500 movies the platform previously offered. Its premium live streaming service, YouTube TV, with more than 100 cable channels, has a decent user interface, app, and recommendation algorithm. YouTube Premium, which includes YouTube Music but not ads, costs $11.99 per month or $119.99 per year. YouTube TV costs $65 per month. YouTube has more than 2 billion monthly logged-in users globally, and YouTube Premium and Music passed the 50-million-user mark in late 2021; YouTube TV had 5 million users as of July 2022, a mix of paid subscribers and users on a free trial. The ad experience on YouTube is terrible, with ad breaks that seem to pop up at random times while you’re watching a video. Average CPM is $16, or $18 for YouTube Select, its premium curated content. YouTube reportedly spent $8.5B on content acquisition in 2019.

Our score:

• UX: 7

• Reach: 9.5

• Market opportunity: 5

• Ad experience: 4

• Value: 5

• Content investment: 7

Total score: 37.5

Honorable mentions: TikTok, Walmart+Paramount, and let’s not forget Quibi.

FAST FOLLOWERS

These are traditional companies entering the streaming fray, primarily through SVOD.

PARAMOUNT+ began life in 2014 as CBS All Access, the live streaming service for CBS programming. It added content from Viacom following their merger, along with content from Paramount Pictures, which inspired the streaming service’s 2021 rebrand. Paramount+ paid subscribers reached 43.3 million in its Q2 2022 earnings report. The company is fond of partnerships for its expansions: It launched in the UK, Ireland, and South Korea with Sky and CJ Entertainment, and it will debut as a hard bundle with Sky Italia in Italy. Paramount also just announced a noteworthy partnership with Walmart that will give Walmart+ members (11.5 million) access to the Paramount+ Essential plan. Paramount+ will spend more than $6 billion on streaming content in 2024, compared to $2.2 billion in 2021, and it plans to also commission 150 international Originals by 2025. The Essential plan, with ads, is $4.99 per month, or $49.99 per year; Essential plan with Showtime is $11.99 per month or $119.99 per year; Premium plan, with no ads and local live CBS stations, is $9.99 per month or $99 per year; and Premium plan with Showtime is $14.99 per month or $149.99 per year. Paramount+ has a high ad load relative to other services, at 17 ads per show or 23.8 per hour.

Our score:

• UX: 8

• Reach: 6

• Market opportunity: 8

• Ad experience: 5

• Value: 9

• Content investment: 6

Total score: 42

DISNEY has had a huge impact on the entertainment industry, and its marquee mascot, Mickey Mouse, is an icon. Its lauded content lineup also includes Star Wars, Pixar, and Marvel. The service’s user experience is seamless and easy to use. When Disney+ launched in 2019, it partnered with Verizon to give 12 months of the service for free to some Verizon customers, more than two-thirds of which kept their subscriptions after the promotional period. Disney+ currently has 152.1 million paid subscribers, although 58.4 are part of its Hotstar partnership in India; its global ARPU is $4.35. Disney will launch its ad-supported service on Dec. 8, 2022 at a cost of $7.99 per month, which is the current price of ad-free Disney+; that will increase to $10.99. Disney will approach ads conservatively on the service, with an average of 4 minutes of ads per hour at launch and zero ads on content aimed at preschoolers. Enthusiasm for the upcoming service contributed to a record $9 billion upfront. Disney planned to spend about $32 billion on content this year, but that includes sports rights, linear, theatrical releases, and its other streaming services; the company specifically spent $2.1 billion on Disney+ content in fiscal Q2. Bonus points for bringing baby Yoda to the world.

Our score:

• UX: 9.5

• Reach: 8

• Market opportunity: 6

• Ad experience: ¯\_(ツ)_/¯

• Value: 8

• Content investment: 7

Cultural impact bonus points: 5

Total score: 43.5

Honorable mentions: HBO Max+Discovery, Peacock.

AVOD PIONEERS

These OGs launched with ad-supported video on demand (AVOD) as their dominant monetization model. They offer a great opportunity for partnerships with any companies that want to entering streaming, such as telcos or a company like Walmart.

TUBI has been free since it was founded in 2014. Since Fox bought the free ad-supported streaming TV (FAST) service in 2020 for $440 million, it has been going gangbusters and is expected to generate $1 billion in annual revenue in the coming years. With a few clicks, it’s pretty easy to start watching content on Tubi across all kinds of devices. Tubi said in May that it would bring on more than 100 original titles in the next 12 months. Its content library includes more than 40,000 titles (lots of B movies), and Tubi offers more than 100 sports and local news channels. Tubi had 51 million active users at the end of 2021, compared to 33 million a year prior. Most of Tubi’s footprint is in the US, but it also operates in Canada, Mexico, New Zealand, and Australia, and it recently expanded to five LatAm countries. The company claims that 27 percent of its users can’t be reached on other AVODs, and 71 percent are unreachable on cable. Its full-screen ads are shown for four to six minutes per hour of viewing; ad pods, with three to five ads, appear every 12-15 minutes. Ads run 6 seconds to 90 seconds.

Our score:

• UX: 8.5

• Reach: 7

• Market opportunity: 6

• Ad experience: 8

• Value: 9

• Content investment: 5

Total: 43.5

ROKU has been called an offspring of Netflix, since Reed Hastings brought Roku founder Anthony Wood on part-time to build a streaming video box for Netflix. When the device’s prospects floundered, Hasting spun it off and gave Wood some cash, employees, patents, and the unfinished device. Thirteen years after Netflix sold its stock in Roku, the company had 63.2 million active accounts, with an ARPU of $44.10, according to its Q2 2022 earnings report. You can buy a Roku streaming device for as little as $30 for the Roku Express, or viewers can access The Roku Channel through the website or mobile app. The Roku Channel has more than 300 free channels covering news, sports, music, and entertainment. Roku reportedly planned to spend $1 billion on content this year, but with its recent earnings missing expectations, the company said that it would slow spending on hiring and content. CPMs for its ad inventory are in the $19-21 range, and its ad load clocks in at seven to eight minutes per hour.

Our score:

• UX: 9

• Reach: 7

• Market opportunity: 5

• Ad experience: 7

• Value: 9

• Content investment: 5

Total score: 42

Honorable mentions: Pluto, IMDBtv/freeve.

Streaming 2.0

After years of Netflix being the main streaming game in town, it seems like everyone is launching or exploring a streaming service of some kind today. But it is so operationally expensive to create new content, update content libraries, acquire new customers, and reacquire old ones. Disney+, Hulu, and ESPN+ collectively lost $1.1 billion in fiscal Q3, exceeding analysts expectations by $300 million; Disney+ probably won’t stop losing money until 2024. Considering that streaming is such a pricey endeavor, how does the Rule of Three play out in five or 10 years? Who's going to survive in this media space? We believe that the next battle in the streaming wars will be between the pure play streamers — such as Netflix, Tubi, and niche providers like MUBI — vs. everyone else, who all have some type of baggage they're dragging into this fight.

Already, we are seeing potential clues for how the streaming wars may play out. There are, for example, doubts about Hulu’s longevity. Disney owns two-thirds of Hulu, with the remainder owned by Comcast. Disney has until January 2024 to buy Comcast’s minority stake for at least $27.5B. Hulu is an awkward fit for Disney now that it has a wildly successful streaming service, and some suspect its value could significantly decline if it simply becomes a small tile within the Disney+ app, reminiscent of how HBO fits within HBO Max.

Speaking of HBO Max, the recent news that it would be merged with Discovery+ next year shows how cutthroat this space can be. The HBO Max app was one of the most downloaded apps in the US earlier this year, and the service was very well received by customers. But with the Warner Bros. Discovery merger, HBO Max will be combined with Discovery+, and several projects such as Batgirl were shelved. The company's goal is to create a deep content library that will provide something for everyone, and with it being very expensive to produce high-quality content, it makes sense to layer in content that's cheaper to make. Discovery+ provides that cheaper content, but this is a significant change in direction toward what appears to be a basic cable-like offering — but without the cable. The company believes that combining all content from both services was the only way to make a viable business, but the value proposition for consumers appears murky to us at best.

And lest we forget, we’ve already seen how even a well-funded endeavor can fail miserably in this space. The short-form, short-lived streaming platform Quibi flamed out in an absurdly short period of time — just 7 months after launch. What makes Quibi interesting is it appeared like the company had the ability to secure the funding needed to launch a streaming service, but it lacked a cogent go-to-market strategy.

Will other streaming services flame out over a longer period of time because they can’t reach the number of subscribers or viewers needed to sustain a profitable service? And are the chances of survival greater for a company that is using streaming to lift other lines of business compared to a pure-play streamer? Only time will tell.

One question

Our rankings still stand a year later (except for that HBO drop); have you made any changes to your streaming lineup recently? If so, who’s in and who’s out?

Dig Deeper

Television Accounts for Less Than Half of U.S. Viewing Time for the First Time

Americans are canceling more streaming plans as prices balloon

Streamflation Is Here and Media Companies Are Betting You’ll Pay Up

Netflix signups remain high, fueled by password-sharing crackdown - data

Why Streaming Services Are Pushing Subscribers to Ad Tiers

Hollywood Studios Disclose Their Offer on Day 113 of Writers’ Strike

Thanks for reading,

Ana, Maja, and the Sparrow team

Enjoyed this piece? Share it, like it, and send us comments (you can reply to this email).

Who we are: Sparrow Advisers

We’re a results oriented management consultancy bringing deep operational expertise to solve strategic and tactical objectives of companies in and around the ad tech and mar tech space.

Our unique perspective rooted deeply in AdTech, MarTech, SaaS, media, entertainment, commerce, software, technology, and services allows us to accelerate your business from strategy to day-to-day execution.

Founded in 2015 by Ana and Maja Milicevic, principals & industry veterans who combined their product, strategy, sales, marketing, and company scaling chops and built the type of consultancy they wish existed when they were in operational roles at industry-leading adtech, martech, and software companies. Now a global team, Sparrow Advisers help solve the most pressing commercial challenges and connect all the necessary dots across people, process, and technology to simplify paths to revenue from strategic vision down to execution. We believe that expertise with fast-changing, emerging technologies at the crossroads of media, technology, creativity, innovation, and commerce are a differentiator and that every company should have access to wise Sherpas who’ve solved complex cross-sectional problems before. Contact us here.